How the Oil Industry Is Planning for the Future

Oil demand is not expected to fall overnight, but there are clear pathways for it to slow and eventually decline. However, how quickly this happens remains highly debated, with major organisations offering very different timelines.

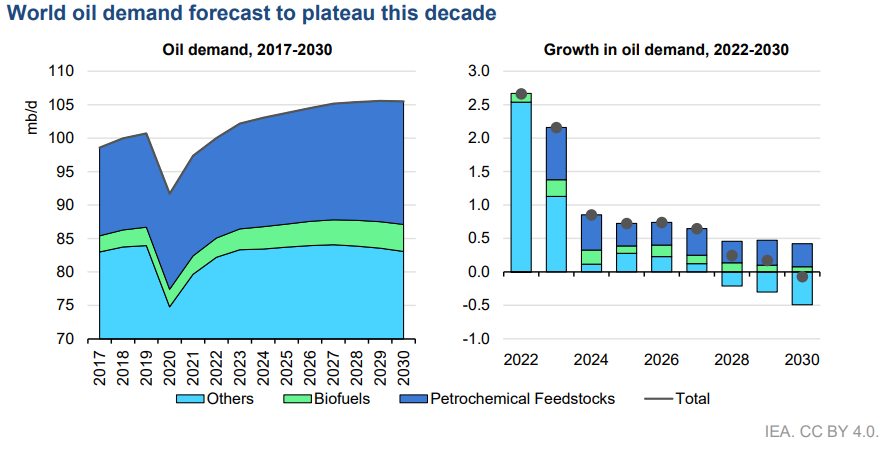

The International Energy Agency expects global oil demand to rise modestly to around 105.5 million barrels per day by 2030, before plateauing by the end of the decade as efficiency improves and alternative technologies expand.

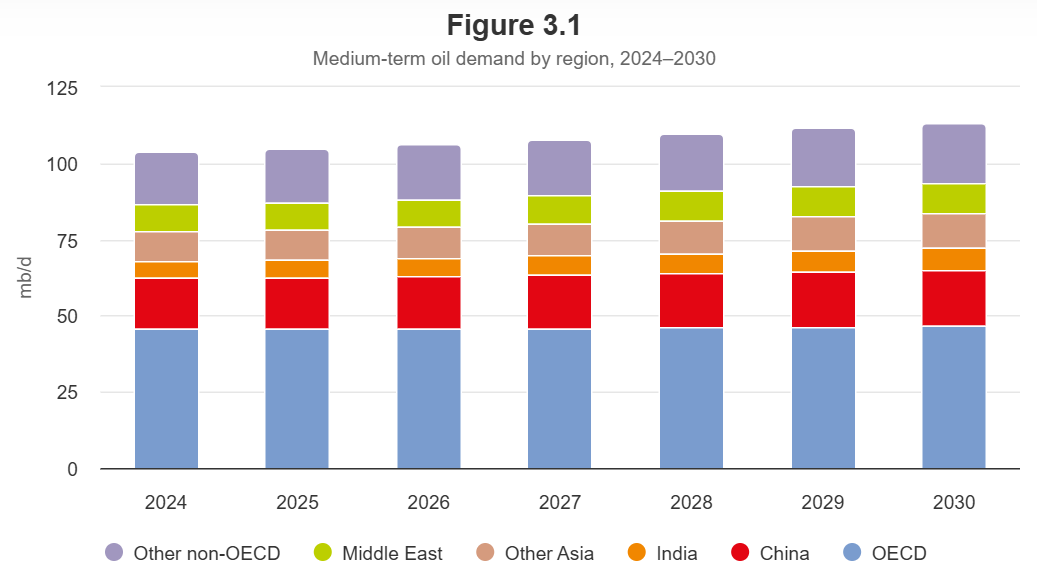

By contrast, OPEC projects continued growth to around 113 million barrels per day by 2030, with demand rising further to nearly 123 million barrels per day by 2050, driven largely by emerging economies.

These differences reflect two key uncertainties: the pace of the energy transition and the strength of demand growth in developing regions, particularly in countries such as India. What is clear, however, is that any shift is likely to be gradual rather than sudden.

One of the main drivers of change is transport. The rise of electric vehicles and improved efficiency is reducing oil use in passenger cars, while oil has already been largely phased out of power generation in many regions. Together, these trends are expected to slow demand growth over time.

At the same time, some sectors remain heavily reliant on oil. Aviation, shipping, and heavy industry continue to depend on liquid fuels, while demand in emerging economies is still growing. This creates a mixed picture, with decline in some areas offset by growth in others.

Another important shift is in how oil is used. Even as fuel demand stabilises, oil remains essential for petrochemicals—used in plastics, fertilisers, and industrial materials—providing a more stable base of demand.

In response, the oil industry is adapting rather than stepping back. A core strategy is to focus on low-cost production, ensuring competitiveness in a slower-growth market. Companies such as Saudi Aramco are positioning themselves to maintain output as higher-cost supply is squeezed out.

At the same time, many firms are expanding into natural gas, widely seen as a lower-emissions alternative to coal. Companies like Shell plc are investing heavily in LNG, expecting gas to play a long-term role in the energy mix.

Some companies are also diversifying into low-carbon energy. Firms including BP and Equinor are investing in renewables, hydrogen, and electricity, although these remain smaller than their core oil and gas businesses.

Alongside this, there is growing focus on reducing emissions from existing operations, including investment in carbon capture technologies. These approaches aim to lower the environmental impact of fossil fuels while allowing continued use in certain sectors.

Overall, the outlook is one of gradual transition. Oil demand may plateau this decade or continue growing for longer, but a rapid decline appears unlikely. Instead, the industry is balancing defending its core business with adapting to a lower-carbon future.